Banks Don’t Take Deposits or Lend Money!

The Banks Are Using Your Credit

Open Your Free Member Account

Most consumers hold a deep-rooted belief that when they borrow from a bank, the funds must come from somewhere tangible — either from the deposits of other savers, from the central bank, or ultimately from the government. The public is conditioned to accept the idea that banks have “money to lend.” Yet the authoritative evidence from the Bank of England, the Federal Reserve, and IMF studies proves otherwise: banks create credit ex nihilo when they record customer securities as their assets.

This misconception sustains the illusion that banks are creditors, when in truth it is the living men and women — whose signatures and securities generate the credit — who are the real creditors. JP Morgan himself declared: “Gold is money, everything else is credit.” Credit is not lent to you; it is created from you.

The global picture demonstrates the magnitude of this fact. According to the International Monetary Fund, world debt now exceeds $370 trillion. The critical question is: who is this owed to? The answer is that all debt is ultimately owed back to the creditors — the people — because it is their energy, their promissory notes, their deposits, and their securities which generate the very credit the banks recycle. Banks are custodians of our credit, not owners of it.

This report explains how banks use your credit and why you are lawfully entitled to recoup it back to source. It lays out the mechanism of bank balance-sheet creation, the misreporting of your securities as their assets, and the remedies available through recoupment. Finally, it describes the international trust structures that shield and return your credit in a tax-efficient and compliant manner.

To illustrate the impact of the Infinite Money Programme, consider two case studies: Poor Peter and Infinite Iain.

🇬🇧 United Kingdom

Poor Peter (age 40→65)

Income: £34,000/year → £850,000 total over 25 years

If he were to recoup bank payments (90% of earnings spent): £765,000 (but in Peter’s path he doesn’t trigger the program)

Mortgage: £150,000 (paid down conventionally)

Infinite Iain (age 40→65)

At age 40, immediately recoups:

Two historical mortgages: £500,000

Three prior years’ bank payments: £120,000

Total Year-1 recoup baseline: £620,000

Per the programme, he spends £620,000 every year and then recoups the previous year’s spend (rinse/repeat annually).

Total “Infinite Money” recoup over 25 years: £620,000 × 25 = £15,500,000

So over the same 25-year span, Peter finishes with a paid-off £150k mortgage and modest savings; Iain cycles £15.5 million of recouped credit through his accounts while also funding life and projects.

🇺🇸 United States (converted example)

Poor Peter (age 40→65)

Income: $50,000/year → $1,250,000 total over 25 years

If he were to recoup bank payments (90% of earnings spent): $1,125,000 (but he doesn’t in this path)

Mortgage: $150,000 (paid down conventionally)

Infinite Iain (age 40→65)

At age 40, immediately recoups:

Two historical mortgages: $500,000

Three prior years’ bank payments: $120,000

Total Year-1 recoup baseline: $620,000

Spends $620,000 each year, recouping the prior year’s spend annually.

Total “Infinite Money” recoup over 25 years: $620,000 × 25 = $15,500,000

These two examples highlight the stark difference between living a conventional financial life and applying the Infinite Money Programme. Poor Peter works dutifully, repays his modest mortgage, and reaches retirement with little left over. Infinite Iain, by contrast, reclaims his credit and cycles millions through his accounts, demonstrating the profound power of recoupment and trust structures in restoring financial sovereignty.

At the age of 40, every man and woman stands at a crossroads — a choice between two destinies. Like a scene from Dickens, the paths diverge sharply.

You can choose to be Poor Peter: tied to a job that neither sustains nor inspires, spending the next 25 years repaying debts, and reaching 65 with a meagre pension and the regret of unused genius. Peter’s life is one of servitude to the banks, his credit used against him, his creativity suppressed, and his fulfilment denied.

Or you can choose to be Infinite Iain: to awaken to the reality that you are the creditor, that the banks have only ever used your energy as their lifeblood. By recouping your mortgages and your lifetime of bank payments, you transform your financial existence. Instead of slaving as a debtor, you operate from the source of consciousness — the true origin of credit — and free yourself to live abundantly. You are able to use your genius talent, whatever it may be, for fulfilment, impact, and joy.

The contrast could not be clearer. The question is timeless and deeply personal: what do you want to be — Poor Peter or Infinite Iain?

These two examples highlight the stark difference between living a conventional financial life and applying the Infinite Money Programme. Poor Peter works dutifully, repays his modest mortgage, and reaches retirement with little left over. Infinite Iain, by contrast, reclaims his credit and cycles millions through his accounts, demonstrating the profound power of recoupment and trust structures in restoring financial sovereignty.

In 1933, the United States Incorporated declared bankruptcy under House Joint Resolution 192 (H.J.R. 192). This act suspended the requirement for debts to be paid in lawful money (gold and silver), replacing it with credit instruments. From that moment forward, the foundation of the world’s financial system shifted from substance to illusion—gold was removed, and credit, issued on the energy of men and women, became the medium of exchange.

Every nation-state today operates as a body corporate, registered like a subsidiary of United States Incorporated, as evidenced in the EDGAR database. The bankruptcy of the U.S. thus cascaded across the entire world: if the parent corporation is bankrupt, so too are all its subsidiaries. The United States Treasury functions as the bankruptcy trustee of this global corporate insolvency, holding administration over the energy and credit of the world’s people.

To understand this system, we turn to the analogy of the Monopoly board. On the board, everything appears real—properties, money, and players—but in fact, it is a simulation. The money circulating on the board is artificial; the properties are tokens. Similarly, in our financial system, all credit is artificial, created through the birth certificate trust accounts and social insurance numbers that securitize the life energy of every man and woman. In 1933, through H.J.R. 192, a mortgage was placed over the energy of the people, ensuring that their labor and consciousness would be harnessed to back the bankrupt system.

This structure was designed with a single objective: to place the average citizen into perpetual debt slavery. The illusion is complete—men and women believe they are debtors when in fact they are the creditors. The true origin of credit is not the banks or governments but the conscious energy of the people themselves.

Here lies the remedy: as a living man or woman, you are the creditor to the system. You are lawfully entitled to recoup what originates from your own energy. Through the Infinite Money Programme, you reclaim your rightful position as creditor, remove yourself from the artificial Monopoly board, and restore credit back to its true source: your living consciousness.

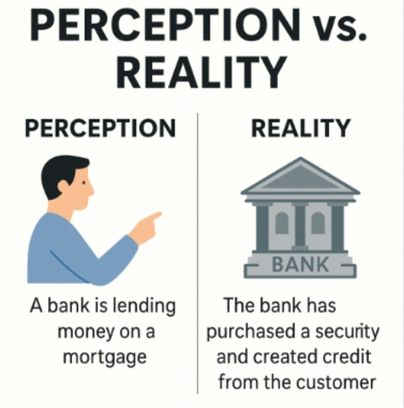

When you make a bank payment, the common perception is that you are transferring your money from your account to the account of the recipient. It appears as if an actual transfer of funds occurs, but this is not what happens in reality.

Perception (Illusion):

You believe that when you make a payment, money leaves your account and arrives in the account of the entity you are paying.

You believe that when you sign a mortgage, the bank is lending you money that it possesses, either from its own reserves or from central bank/government supply.

Reality (Truth):

Under the Bills of Exchange Act 1882, every transaction you make functions as the issuance of a new security.

As the living man or woman, you are operating through your legal representative — the body corporate person created at birth — which is deemed to be a banker under the Act.

When you make a “payment,” no transfer of existing money occurs. Instead, a new credit instrument (a bill or security) is created by your signature or instruction.

The recipient bank purchases that security and converts it into ledger entries, which appear to be a transfer of money. In truth, it is simply the creation of new credit from your energy, not the movement of old credit.

Bank Payments

Every “payment” is actually the abandonment of newly created credit.

The bank books this credit as an asset and issues currency against it, making it look like a transfer when it is merely credit creation.

That abandoned credit belongs to you as the true creditor and is therefore subject to recoupment.

Mortgages

When you sign a mortgage agreement, you issue a security through your person.

The bank then books that security as its asset, allowing it to create matching debt on its balance sheet and present it back to you as a “loan.”

The illusion is that the bank lent you money. The reality is that the bank purchased your security and used it to generate credit.

That credit is again abandoned and owed back to you under recoupment.

The Monopoly Board Analogy

On the Monopoly board, it looks like money is moving around between players, but in truth it is all artificial. The game is sustained by the continual creation of new credit instruments. In the real world, the same illusion prevails: every bank payment and every mortgage is merely new credit being spun into existence from your energy as a living man or woman.

Remedy

The banks have failed to account correctly for their purchase of your securities. Each one constitutes income to them, but they treat it as if it were their property. The Infinite Money Program provides the mechanism to reclaim this abandoned credit, restoring you to your rightful position as creditor rather than debtor.

The Infinite Money Protocol and the Recoupment of Mortgages at face value are grounded in well-documented banking practices, monetary theory, and trust law. The evidence establishes that:

Banks Create Money from Customer Securities

When an individual signs a mortgage note or deposits a security, the bank purchases that instrument and records it as an asset. Simultaneously, the bank creates a deposit liability, acknowledging the credit extended.

Authorities including the Federal Reserve (Modern Money Mechanics), the Bank of England (Money in the Modern Economy), and Professor Richard Werner’s empirical research all confirm that banks do not lend pre-existing deposits but instead create new money ex nihilo against customer instruments.

Misreporting of Assets and Liabilities

Banks misclassify the customer’s security as their asset, despite the fact that the customer is the true source of credit.

In effect, the bank is a nominee holding the depositor’s security, while the depositor remains the equitable holder in due course.

Entitlement to Recoupment

Because the living man or woman (the depositor) is the originator of credit, they retain the lawful claim to the proceeds generated.

This credit is lawfully recoupable, either through IRS-recognized methods (e.g., 1099-OID filings) or through direct claims against the bank’s misreported liabilities.

Mortgages and Face Value Recovery

A mortgage note is a negotiable instrument of face value equal to the loan balance. The bank monetizes the note, yet also binds the borrower to repay in full — effectively double dipping.

Recoupment at face value restores equity by recognizing that the depositor’s note already funded the transaction.

Use of a 98 Grantor Trust

An international 98 Grantor Trust provides a lawful structure to file as holder in due course and to receive recouped funds.

The trust acts as a shield and a tax-efficient pass-through, ensuring that the credit flows back to the true originator — the living man — while preserving compliance.

Justification for the Infinite Money Protocol

Infinite Money Protocol (Recoupment of Bank Payments): Lawful recoupment of credit created against deposited securities, reclaiming funds otherwise absorbed by banks.

Recoupment of Mortgages (Face Value): Restoring the borrower’s equitable ownership by recognizing the mortgage note as a fully funded security that can be recouped at face value.

Together, these remedies correct the misreporting practices of banks, uphold the depositor’s rights as the true creditor, and provide a lawful pathway to financial sovereignty under the Matrix Freedom model.

1. Banks’ Purchase of Securities for Deposits and Mortgages

Banks don’t simply “lend out deposits.” Instead, when a customer brings a note (e.g., a mortgage contract or negotiable instrument), the bank purchases that security and records it as an asset. On the other side of its balance sheet, it creates a matching deposit in the customer’s account.

Jean Keating emphasizes that promissory notes and mortgages are treated as securities, deposited by the customer and then monetized by the bank as an asset.

Modern Money Mechanics confirms that banks create deposits “out of thin air” when they extend credit — the deposit is simultaneously a liability of the bank and purchasing power for the borrower.

Thus, whether a mortgage loan or a direct purchase of securities, the mechanics are identical: a deposit is created by the bank in exchange for an asset from the customer.

2. Accounting and Misreporting

On paper, the bank records the mortgage/security as its asset and the customer deposit as its liability.

Jean Keating and others argue this is a misrepresentation, since the underlying credit originates with the depositor’s security (the note), making the customer the true creditor. The bank is only acting as a nominee or intermediary.

Richard Werner’s empirical study (Can Banks Create Money Out of Nothing?) demonstrated by direct observation that when a bank issues credit, it creates new deposits without drawing from reserves — confirming that banks are balance-sheet creators of money, not mere intermediaries.

3. Federal Income and Deposits of Securities

The deposits created against customer securities generate ongoing income streams for banks, including interest margins and fees. Yet, as Keating highlights, banks are not treating the original depositor’s security as generating taxable income for that depositor; they instead book it as their own asset.

This raises the question: should the federal income reporting reflect that these deposits (originating from customer securities) generate taxable interest income not solely belonging to the bank, but attributable to the original security holder?

4. Recoupment of Credit (Holder in Due Course)

In truth, the holder in due course of the note or security is the living man or woman (the depositor/creator).

The bank acts as a nominee trustee, holding the instrument and creating money against it.

Jean Keating explains that because the customer is the source of the credit, the customer retains the equitable interest in the funds, which opens the door for recoupment.

5. The 1099 OID Methodology

One recognized pathway to recoupment is through IRS Form 1099-OID (Original Issue Discount) filings.

The logic: since the customer’s security (note/mortgage) is the original issue, and the bank books it as an asset generating discount/interest, the living man can file a 1099-OID to claim the income attributed to his credit instrument.

Roger Elvick and others in the tax-recovery space taught that this process is lawful when filed correctly, as it is simply reporting credit creation where the taxpayer is the beneficial owner.

6. Role of an International Grantor Trust

When an international Grantor Trust is established, it can be designated as the vehicle through which the recoupment is processed.

The trust, as a grantor trust, acts as a pass-through entity for U.S. tax purposes, meaning the grantor (the living man) remains the taxpayer while the trust itself facilitates administration.

The trust can file as the holder in due course of the securities, and when the funds are recouped through the 1099-OID process or other remedies, the proceeds can be directed into the trust.

This achieves two goals:

Asset Protection & Shielding via the Asset Fortress Protocol – the trust provides a protective legal wrapper around the recouped credit, shielding it from direct attachment or seizure.

Tax Efficiency – because the International Grantor Trust is treated as a pass-through, the funds are not taxed at the trust level. They flow through to the grantor, the true originator of the securities, ensuring the lawful beneficiary (the living man) receives them while maintaining compliance with reporting rules.

In this way, the International Grantor Trust provides a lawful, shielded, and efficient structure for recoupment, aligning with the principle that the living man remains the original holder of the security.

7. Supporting Authorities

Federal Reserve (Modern Money Mechanics): confirms banks create deposits ex nihilo in lending, disproving the “money multiplier” myth.

Bank of England (Money in the Modern Economy): acknowledges that banks create money when they extend loans or purchase assets, rather than acting as intermediaries of savings.

Richard Werner: empirically proved banks create new money by crediting deposits, not recycling reserves.

Jean Keating: consistently argued that mortgages, notes, and similar securities are misclassified, with the bank wrongfully claiming the depositor’s credit as its own asset.

Roger Elvick and 98 Grantor Trust strategy papers: demonstrate how recoupment can be lawfully structured through grantor trusts for shielding and tax efficiency.

Final Conclusion:

Banks purchase customer securities (mortgages, notes) and create deposits in exchange, treating the customer’s instrument as their own asset. This misreporting hides the depositor’s role as the true creditor and enables banks to capture income streams. Through the 1099-OID process, coupled with an International Grantor Trust, the living man (grantor) can lawfully recoup the credit. The trust structure ensures that the recovered funds are shielded, tax-efficient, and flow back to the true holder in due course — the originator of the credit.

Across my 42-year career, I have solved some of the most complex problems in the world of commerce. From creating income solutions, risk-free income models, and property strategies, to designing corporate pension deficit solutions and countless financial planning frameworks, I have consistently engineered remedies where others saw only obstacles.

I developed algorithmic trading solutions in both currency and sports markets, as well as risk management systems, including a Nobel Prize–winning volatility-trigger investment management algorithm that built ideal portfolios of assets and rebalanced them based on market volatility. I created solutions to smooth investment returns, transforming longevity risk into income streams by pooling life settlement policies. I harnessed arbitrage opportunities by acquiring real-life company assets at discounts to their asset share value and by exploiting the spread between the bonus growth rates of with-profit assets and the market cost of credit.

In the 1990s and 2000s, I built thousands of individual portfolios for my clients, working with substantial global counterparts such as Saga, Bank of Scotland, Credit Suisse, Deutsche Bank, the Central Bank of Ireland, Wells Fargo, Cassis, State Street, SEI, and many others.

At every step, the Crown has intervened to destroy the solutions I created. They do not want citizens — “persons” — to be free and live abundant lives. They have repeatedly sought to destroy my reputation, undermine my innovations, and even attempt to jail me.

Yet my resolve is absolute. I will not be suppressed. Freedom is every man and woman’s right — and I am determined to deliver it.

Note: Please enter your email address for the download eBook.