A peaceful way to exit your mortgage and free your home by recouping the credit you created

Open Your Free Member Account

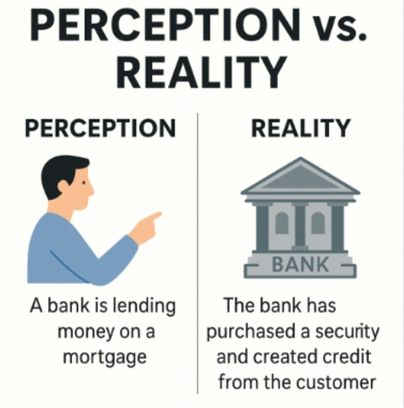

Banks use your credit to create “loans” and “mortgages” Now you can recoup your credit, redeem the mortgage in fiat, release the mortgage charge, and then recoup that redemption payment too—quietly, lawfully, and without a war with the mortgage market.

Download eBook – The banks are using your credit and how to recoup it

Recoup the face value of mortgages and bank payments.

Most people who try to exit a mortgage go to war: they argue bad signatures, securitisation, fraud, “no consideration,” and then spend months (or years) in litigation. If they stop paying, foreclosure looms—and the bank takes the property anyway.

The Calm Alternative: Mortgage Liberation

Play the Monopoly game more intelligently—peacefully, administratively.

Recoup the credit that originally created your mortgage.

Redeem the account in fiat so the servicer willingly removes the charge.

Recoup the redemption payment as part of your annual cycle.

Recycle year on year to build financial abundance.

No courtroom fights. No brinkmanship. You’re using the system exactly as it’s designed—so everyone in the chain cooperates.

Peace is best: Recoup → Redeem → Recoup → Repeat.

In 1933, the United States Incorporated declared bankruptcy under House Joint Resolution 192 (H.J.R. 192). This act suspended the requirement for debts to be paid in lawful money (gold and silver), replacing it with credit instruments. From that moment forward, the foundation of the world’s financial system shifted from substance to illusion—gold was removed, and credit, issued on the energy of men and women, became the medium of exchange.

Every nation-state today operates as a body corporate, registered like a subsidiary of United States Incorporated, as evidenced in the EDGAR database. The bankruptcy of the U.S. thus cascaded across the entire world: if the parent corporation is bankrupt, so too are all its subsidiaries. The United States Treasury functions as the bankruptcy trustee of this global corporate insolvency, holding administration over the energy and credit of the world’s people.

To understand this system, we turn to the analogy of the Monopoly board. On the board, everything appears real—properties, money, and players—but in fact, it is a simulation. The money circulating on the board is artificial; the properties are tokens. Similarly, in our financial system, all credit is artificial, created through the birth certificate trust accounts and social insurance numbers that securitize the life energy of every man and woman. In 1933, through H.J.R. 192, a mortgage was placed over the energy of the people, ensuring that their labor and consciousness would be harnessed to back the bankrupt system.

This structure was designed with a single objective: to place the average citizen into perpetual debt slavery. The illusion is complete—men and women believe they are debtors when in fact they are the creditors. The true origin of credit is not the banks or governments but the conscious energy of the people themselves.

Here lies the remedy: as a living man or woman, you are the creditor to the system. You are lawfully entitled to recoup what originates from your own energy. Through the Infinite Money Programme, you reclaim your rightful position as creditor, remove yourself from the artificial Monopoly board, and restore credit back to its true source: your living consciousness.

New video inside: How to recoup historic mortgages (2001 onward) and use that recoupment to redeem, then recoup the redemption.

In commercial law, the true holder in due course of a mortgage note or security is not the bank, but the living man or woman — the depositor and original creator of the instrument.

The bank acts merely as a nominee trustee. It takes custody of the note, securitizes it, and creates deposits against it.

As Jean Keating explained, because the borrower is the source of the credit, the borrower retains the equitable interest in both the instrument and the funds derived from it.

This establishes the borrower’s standing to recoup the full face value of the security that the bank wrongfully claimed.

1. The 1099-OID Methodology

One lawful, IRS-recognized pathway to enforce recoupment is the 1099-OID (Original Issue Discount) process:

The logic:

The mortgage note is the original issue security, created by the living man.

The bank books this security as its asset and generates income (interest/discount) from it.

Since the originator (the depositor) is the rightful holder in due course, they may file a 1099-OID to report and reclaim the income and discount attributable to their credit.

Authorities & Precedent:

Roger Elvick and others demonstrated that correctly filed OID returns are not tax evasion but accurate reporting of credit creation where the living man is the beneficial owner.

When executed in sequence with proper notices, this process becomes an enforcement mechanism, forcing recognition of the depositor’s beneficial interest.

2. Role of the International Grantor Trust

To maximize protection and efficiency, the recoupment process is administered through an international Grantor Trust:

Pass-Through Structure:

Under U.S. tax rules, a Grantor Trust is a pass-through entity.

The trust itself does not bear tax; instead, all income flows directly to the grantor — the living man — who remains the taxpayer.

Benefits of the Trust:

Asset Protection & Shielding – The trust provides a protective legal wrapper. Recouped credit is shielded from direct seizure, liens, or attachment, ensuring the funds remain beyond reach of creditors or hostile entities.

Tax Efficiency – Because it is treated as transparent for tax purposes, the trust avoids double taxation. Funds pass directly to the grantor while maintaining full compliance with reporting rules.

Lawful Standing – The trust can file and act as the holder in due course on behalf of the depositor, streamlining administration and providing an institutional face for enforcement.

In practice:

The 1099-OID filings are executed through the Grantor Trust.

Once funds are recouped, they flow into the trust, where they are shielded, managed, and distributed lawfully back to the living man.

No. The calm path avoids confrontation. You redeem the account in fiat; the servicer releases the charge. Then you recoup that redemption payment inside your normal cycle.

The old route tried to prove void/ab initio. The calm route sidesteps the fight: recoup → redeem → recoup, with the same end—a liberated home.

The calm path can still apply. Redeeming the account moots the enforcement; we also provide a court-stage pack for pausing escalation while you complete redemption. (See member area.)

No—education only. We encourage professional advice for filings, trust setup, and local compliance.

Note: Please enter your email address for the download eBook.