Banks Don’t Take Deposits or Lend Money!

The Banks Are Using Your Credit

Open Your Free Member Account

Across the world millions of mortgages have been created not by banks “lending money” but by the living man or woman themselves — operating through the body corporate as a public banker under the Bills of Exchange Act 1882. The borrower’s signature on the mortgage note is the security that funds the transaction. It is this act — the transfer of energy into a negotiable instrument — that creates the asset the bank records on its balance sheet.

As Professor Richard Werner demonstrated in his empirical studies, banks do not lend out deposits or reserves; they create credit ex nihilo the moment they receive a signed note. The mortgage provider purchases the borrower’s security, books it as an asset, and simultaneously creates a matching liability in the form of a deposit credited back to the “borrower.” The illusion is that the bank lent money. The reality is that the borrower’s own credit was monetised and returned as a so-called “loan.”

From here the deception compounds:

Mortgages are bundled into securitisations and sold to investment banks.

These bundles are traded for multiples of their face value, generating vast profits.

Income streams from repayments are sliced and sold to investors.

Meanwhile, the living creditor — the man or woman who created the credit — is misreported as a debtor.

The fiduciary at the top of this system, the Indentured Trustee, compounds the fraud by misaccounting the bank as beneficiary when, in law, the true beneficiary is the living creditor. This is the essence of modern financial slavery: mortgages created from nothing, securitised into global markets, and enforced against the very people who generated the credit.

The Mortgage Redemption Protocol exposes this illusion and provides the pathway to redeem mortgages by asserting the creditor’s lawful position and collapsing the fraudulent presumption.

1. How Mortgages Are Really Created

Bills of Exchange Act 1882: The mortgage note signed by the alleged borrower is a negotiable instrument, deemed a Bill of Exchange.

Bank Balance Sheet Trick:

Security signed by borrower = booked as bank asset.

Matching deposit = bank liability credited as “loan.”

Professor Richard Werner: Confirmed empirically that loans are not funded by reserves but by credit creation against customer securities.

Implication: The borrower is the originator of the credit; the bank is merely a recorder and mis-accountant.

2. Securitisation: The Big Short Exposed

Like the film The Big Short illustrated, mortgage notes are not held on bank balance sheets:

They are bundled into Mortgage-Backed Securities (MBS).

Sold to investment banks who trade them globally.

Repayment streams are securitised into derivative products, sold multiple times over.

The Indentured Trustee misreports the bank as beneficiary, even though the credit originated with the living man or woman.

Result: The bank profits many times over from a mortgage “created out of nothing,” while the borrower is trapped paying instalments on what was already funded by their own credit.

3. The Accounting Deception

The entire mortgage system rests on double-dipping:

The bank books the borrower’s note as its asset.

It creates a liability back to the borrower, claiming to have lent money.

It then securitises and sells the note, multiplying profit streams.

Meanwhile, it enforces monthly repayments as if the note were still an unpaid debt.

This inversion — treating the creditor as debtor — is the core of the fraud.

4. Mortgage Redemption

The Mortgage Redemption Protocol adapts the Infinite Money framework to mortgages specifically:

The Mortgage Redemption Protocol applies to mortgages that have already been discharged by the alleged borrower, but remain fraudulently enforced by banks. The key lies in correcting the accounting through the Original Issue Discount (OID) mechanism.

When a mortgage is created, the borrower’s note is treated as a security purchased by the bank. This instrument generates taxable income, yet banks and indentured trustees routinely fail to report it correctly. Instead, they misclassify themselves as the beneficiaries, concealing the true creditor.

Redemption occurs when the OID income is properly reported through an International Grantor Trust acting as holder in due course. By filing the appropriate returns, the trust reclaims the federal income that should have been attributed to the living man from the outset. Once this reporting is made, the credit is lawfully redirected back to source — the living man or woman, operating as agent for the body corporate.

In this way, the Mortgage Redemption Protocol collapses the misreporting, forces recognition of the true creditor, and ensures that discharged mortgages are redeemed in both law and equity.

5. International Trust Shield

As with the Infinite Money Protocol, redemption requires lawful structures:

International Grantor Trusts: Acts as a passthrough entity to the holder in due course to receive recouped funds.

Tax-Efficient Shield: Credit is returned to the living man through trust pass-through.

Jurisdictional Protection: Trust law removes funds from Crown jurisdiction and prevents further misappropriation.

Conclusion

Mortgages are an accounting illusion — securities created by the living man or woman, misreported as bank assets, bundled into securitisations, and enforced against the originator as if they were debtor. The Mortgage Redemption Protocol restores equity by recognising the living man or woman as the true creditor, redeeming the mortgage, and collapsing the slavery system of endless instalments.

Through notices, bills of exchange, fiduciary enforcement, and trust structures, the Protocol provides a practical pathway to discharge mortgages and recoup the value wrongfully diverted to banks.

To illustrate the impact of the Mortgage Redemption Protocol, consider two case studies — one man who leaves his discharged mortgages as abandoned credit, and another who redeems them as holder in due course.

🇬🇧 United Kingdom

Poor Peter (age 40 → 90)

Has discharged three mortgages worth £1,000,000 in total.

Forgets, or never realises, that he remains the holder in due course of this credit.

Like a forgotten bank account with £1 million still on deposit, Peter simply leaves the credit abandoned.

The banks continue to profit endlessly from his securities — through securitisation, trading, and income streams — while Peter gains nothing.

At age 90, Peter finishes life with no recovery of his credit, having unknowingly subsidised the banking system for 50 years.

Infinite Iain (age 40 → 90)

Recognises that he is the holder in due course of £1,000,000 in previously discharged mortgages.

Invokes the Mortgage Redemption Protocol, recoups the £1,000,000, and begins spending it.

Each year, he recoups what he spent the previous year, creating a cycle of continuous redemption.

Over 50 years (age 40 → 90), Iain recoups £1,000,000 annually × 50 years = £50,000,000.

He lives abundantly, using his own credit rather than leaving it to be exploited by the banks.

At the age of 40, every man and woman stands at a crossroads — a choice between two destinies. Like a scene from Dickens, the paths diverge sharply.

You can choose to be Poor Peter: tied to a job that neither sustains nor inspires, spending the next 50 years repaying debts, and reaching 90 living from a meagre pension or universal credit and the regret of unused genius. Peter’s life is one of servitude to the banks, his credit used against him, his creativity suppressed, and his fulfilment denied.

Or you can choose to be Infinite Iain: to awaken to the reality that you are the creditor, that the banks have only ever used your energy as their lifeblood. By recouping your mortgages and your lifetime of bank payments, you transform your financial existence. Instead of slaving as a debtor, you operate from the source of consciousness — the true origin of credit — and free yourself to live abundantly. You are able to use your genius talent, whatever it may be, for fulfilment, impact, and joy.

The contrast could not be clearer. The question is timeless and deeply personal: what do you want to be — Poor Peter or Infinite Iain?

In 1933, the United States Incorporated declared bankruptcy under House Joint Resolution 192 (H.J.R. 192). This act suspended the requirement for debts to be paid in lawful money (gold and silver), replacing it with credit instruments. From that moment forward, the foundation of the world’s financial system shifted from substance to illusion—gold was removed, and credit, issued on the energy of men and women, became the medium of exchange.

Every nation-state today operates as a body corporate, registered like a subsidiary of United States Incorporated, as evidenced in the EDGAR database. The bankruptcy of the U.S. thus cascaded across the entire world: if the parent corporation is bankrupt, so too are all its subsidiaries. The United States Treasury functions as the bankruptcy trustee of this global corporate insolvency, holding administration over the energy and credit of the world’s people.

To understand this system, we turn to the analogy of the Monopoly board. On the board, everything appears real—properties, money, and players—but in fact, it is a simulation. The money circulating on the board is artificial; the properties are tokens. Similarly, in our financial system, all credit is artificial, created through the birth certificate trust accounts and social insurance numbers that securitize the life energy of every man and woman. In 1933, through H.J.R. 192, a mortgage was placed over the energy of the people, ensuring that their labor and consciousness would be harnessed to back the bankrupt system.

This structure was designed with a single objective: to place the average citizen into perpetual debt slavery. The illusion is complete—men and women believe they are debtors when in fact they are the creditors. The true origin of credit is not the banks or governments but the conscious energy of the people themselves.

Here lies the remedy: as a living man or woman, you are the creditor to the system. You are lawfully entitled to recoup what originates from your own energy. Through the Infinite Money Programme, you reclaim your rightful position as creditor, remove yourself from the artificial Monopoly board, and restore credit back to its true source: your living consciousness.

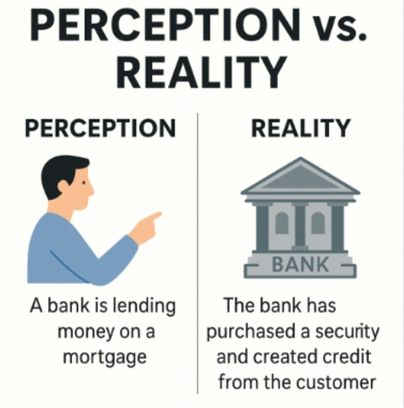

When you take out a mortgage, the common perception is that the bank lends you money from its reserves or deposits. It appears as though the bank advances existing funds which you must then repay with interest. But this is not what happens in reality.

Perception (Illusion):

You believe the bank already possesses the funds it is lending, either from depositors, reserves, or central bank facilities.

You believe you are borrowing the bank’s money and are therefore indebted to it for the principal plus interest.

You believe the mortgage contract is evidence of a loan advanced to you, rather than a credit instrument issued by you.

Reality (Truth):

Under the Bills of Exchange Act 1882, the mortgage agreement you sign is itself a bill of exchange — a negotiable instrument created by your signature.

That signed instrument is deposited with the bank. The bank immediately books it as an asset on its balance sheet.

Against this new “asset,” the bank creates a matching deposit liability, which is credited back to your account and presented as a “loan.”

No pre-existing money was lent. The bank simply monetised your bill of exchange and mirrored it back to you as debt.

Bank Accounting Deception

The bank’s records show your signed mortgage note as their asset, when in fact it was your credit that created the value.

This false accounting makes the bank appear as lender and you as borrower, reversing the true roles of creditor and debtor.

The bank then earns interest on this fabricated liability, while concealing that the original funding came entirely from your security.

Securitisation and Sale of the Security

Once deposited, mortgage notes are not kept on the bank’s books. They are bundled into securitisations and sold on to investment banks.

These bundles are then traded as mortgage-backed securities (MBS), often for multiples of their face value.

The repayment streams (your monthly instalments) are sliced, sold, and leveraged across global financial markets.

Meanwhile, the Indentured Trustee overseeing the securitisation misreports the beneficiary as the bank or nominee investors, instead of recognising you — the originator of credit — as the true beneficiary.

The Monopoly Board Analogy

Just as on the Monopoly board, it looks like money is moving between players, but in truth it is artificial.

The mortgage note you sign is the “property card.”

The bank books it as its own and then trades it across the board.

You, the true creator of credit, are left paying instalments on an illusion.

The entire system is sustained by continual creation and sale of new credit instruments, not by the lending of existing money.

Remedy

The fraud lies in the bank’s failure to correctly account for your mortgage note as your credit. Instead of treating it as income belonging to you, the bank appropriates it as its property, securitises it, and profits many times over.

The Mortgage Redemption Protocol provides the pathway to reverse this deception. By recognising yourself as the holder in due course of the bill of exchange, and by applying notice, estoppel, and redemption processes, you can reclaim your credit, discharge the mortgage, and restore yourself to your rightful position as creditor — rather than debtor.

The Mortgage Redemption Protocol and the recoupment of Mortgages at face value are grounded in well-documented banking practices, monetary theory, and trust law. The evidence establishes that:

Banks Create Money from Customer Securities

When an individual signs a mortgage note or deposits a security, the bank purchases that instrument and records it as an asset. Simultaneously, the bank creates a deposit liability, acknowledging the credit extended.

Authorities including the Federal Reserve (Modern Money Mechanics), the Bank of England (Money in the Modern Economy), and Professor Richard Werner’s empirical research all confirm that banks do not lend pre-existing deposits but instead create new money ex nihilo against customer instruments.

Misreporting of Assets and Liabilities

Banks misclassify the customer’s security as their asset, despite the fact that the customer is the true source of credit.

In effect, the bank is a nominee holding the depositor’s security, while the depositor remains the equitable holder in due course.

Entitlement to Recoupment

Because the living man or woman (the depositor) is the originator of credit, they retain the lawful claim to the proceeds generated.

This credit is lawfully recoupable, either through IRS-recognized methods (e.g., 1099-OID filings) or through direct claims against the bank’s misreported liabilities.

Mortgages and Face Value Recovery

A mortgage note is a negotiable instrument of face value equal to the loan balance. The bank monetizes the note, yet also binds the borrower to repay in full — effectively double dipping.

Recoupment at face value restores equity by recognizing that the depositor’s note already funded the transaction.

Use of an International Grantor Trust

An International Grantor Trust provides a lawful structure to file as holder in due course and to receive recouped funds.

The trust acts as a shield and a tax-efficient pass-through, ensuring that the credit flows back to the true originator — the living man — while preserving compliance.

Accounting and Misreporting

On paper, the bank records the mortgage/security as its asset and the customer deposit as its liability.

Jean Keating and others argue this is a misrepresentation, since the underlying credit originates with the depositor’s security (the note), making the customer the true creditor. The bank is only acting as a nominee or intermediary.

Richard Werner’s empirical study (Can Banks Create Money Out of Nothing?) demonstrated by direct observation that when a bank issues credit, it creates new deposits without drawing from reserves — confirming that banks are balance-sheet creators of money, not mere intermediaries.

Federal Income and Deposits of Securities

The deposits created against customer securities generate ongoing income streams for banks, including interest margins and fees. Yet, as Keating highlights, banks are not treating the original depositor’s security as generating taxable income for that depositor; they instead book it as their own asset.

This raises the question: should the federal income reporting reflect that these deposits (originating from customer securities) generate taxable interest income not solely belonging to the bank, but attributable to the original security holder?

Recoupment of Credit (Holder in Due Course)

In truth, the holder in due course of the note or security is the living man or woman (the depositor/creator).

The bank acts as a nominee trustee, holding the instrument and creating money against it.

Jean Keating explains that because the customer is the source of the credit, the customer retains the equitable interest in the funds, which opens the door for recoupment.

The 1099 OID Methodology

One recognised pathway to recoupment is through IRS Form 1099-OID (Original Issue Discount) filings.

The logic: since the customer’s security (note/mortgage) is the original issue, and the bank books it as an asset generating discount/interest, the living man can file a 1099-OID to claim the income attributed to his credit instrument.

Roger Elvick and others in the tax-recovery space taught that this process is lawful when filed correctly, as it is simply reporting credit creation where the taxpayer is the beneficial owner.

Role of an International Grantor Trust

When an International Grantor Trust is established, it can be designated as the vehicle through which the recoupment is processed.

The trust, acts as a pass-through entity for U.S. tax purposes, meaning the grantor (the living man as agent for the body corporate person) remains the taxpayer while the trust itself facilitates administration.

The trust can file as the holder in due course of the securities, and when the funds are recouped through the 1099-OID process or other remedies, the proceeds can be directed into the trust.

This achieves two goals:

Asset Protection & Shielding via the Asset Fortress Protocol – the trust provides a protective legal wrapper around the recouped credit, shielding it from direct attachment or seizure.

Tax Efficiency – because the International Grantor Trust is treated as a pass-through, the funds are not taxed at the trust level. They flow through to the grantor, the true originator of the securities, ensuring the lawful beneficiary (the living man) receives them while maintaining compliance with reporting rules.

In this way, the International Grantor Trust provides a lawful, shielded, and efficient structure for recoupment, aligning with the principle that the living man remains the original holder of the security.

Supporting Authorities

Federal Reserve (Modern Money Mechanics): confirms banks create deposits ex nihilo in lending, disproving the “money multiplier” myth.

Bank of England (Money in the Modern Economy): acknowledges that banks create money when they extend loans or purchase assets, rather than acting as intermediaries of savings.

Richard Werner: empirically proved banks create new money by crediting deposits, not recycling reserves.

Jean Keating: consistently argued that mortgages, notes, and similar securities are misclassified, with the bank wrongfully claiming the depositor’s credit as its own asset.

Roger Elvick trust strategy papers: demonstrate how recoupment can be lawfully structured through grantor trusts for shielding and tax efficiency.

Final Conclusion:

Banks purchase customer securities (mortgages, notes) and create deposits in exchange, treating the customer’s instrument as their own asset. This misreporting hides the depositor’s role as the true creditor and enables banks to capture income streams. Through the 1099-OID process, coupled with an International Grantor Trust, the living man (grantor) can lawfully recoup the credit. The trust structure ensures that the recovered funds are shielded, tax-efficient, and flow back to the true holder in due course — the originator of the credit.

Across my 42-year career, I have solved some of the most complex problems in the world of commerce. From creating income solutions, risk-free income models, and property strategies, to designing corporate pension deficit solutions and countless financial planning frameworks, I have consistently engineered remedies where others saw only obstacles.

I developed algorithmic trading solutions in both currency and sports markets, as well as risk management systems, including a Nobel Prize–winning volatility-trigger investment management algorithm that built ideal portfolios of assets and rebalanced them based on market volatility. I created solutions to smooth investment returns, transforming longevity risk into income streams by pooling life settlement policies. I harnessed arbitrage opportunities by acquiring real-life company assets at discounts to their asset share value and by exploiting the spread between the bonus growth rates of with-profit assets and the market cost of credit.

In the 1990s and 2000s, I built thousands of individual portfolios for my clients, working with substantial global counterparts such as Saga, Bank of Scotland, Credit Suisse, Deutsche Bank, the Central Bank of Ireland, Wells Fargo, Cassis, State Street, SEI, and many others.

At every step, the Crown has intervened to destroy the solutions I created. They do not want citizens — “persons” — to be free and live abundant lives. They have repeatedly sought to destroy my reputation, undermine my innovations, and even attempt to jail me.

Yet my resolve is absolute. I will not be suppressed. Freedom is every man and woman’s right — and I am determined to deliver it.

Note: Please enter your email address for the download eBook.